Mortgage Market Review

What Is Likely To Happen to Mortgage Rates and House Prices in 2023?

Introduction

A belated Happy New Year to you all. We've been preparing a market update since the start of the year but have delayed until the all-important UK inflation figures were released. The inflation data is the key factor in the Bank of England’s (BOE) interest rate setting committee, and the level of the BOE base rate and the direction it is heading correlates to mortgage rates the level of which is a key determinate of house prices.To summarise 2022, it was a year of two halves, in the first half the market was flying with demand way outstripping supply and most properties going for over asking price, the tide turned in July when it became clear that interest rates were going to have to rise much further than anticipated. By the time Truss / Kwarteng took over best buy fixed rates had already increased by 2% since the start of the year, and after the mini budget the panic that ensued in the mortgage market drained what sentiment was left in the housing market. Fast forward three months and mortgage rates have settled in the mid 4s, and the housing market is now in the hands of buyers with sellers having to reset their price expectations to achieve a sale.

Bank of England Base Rate

In my November update I suggested that the base rate would peak in a range of 4%-4.5%. Wednesday’s positive news on inflation which confirms it has peaked and will likely fall significantly this year given that wholesale gas and oil prices have greatly reduced suggest to me that the BOE base rate will top out at 4.25% in this cycle, with my best guess being either a 0.25% or 0.50% rise in February and another one or two increases of 0.25% at the March and May MPC meetings.

Beyond this I feel the BOE will pause for at least six months, but should inflation fall back towards its long- term target of 2% they may then cut base rate in the final months of the year / early 2024 to help stimulate the Economy. My prediction for where base rate will end this year is in the range of 3.5%-4% and by the end of 2024 in the range of 3%-3.5%. Our advice to borrowers to opt for base rate trackers in Q4 2022 that were routinely available at 0.30% above base rate compared to fixed rates above 5.5% has proved to

be correct, and we will be contacting all clients on tracker rates once fixed rates fall to a more appealing level later this year.

Mortgage Rates

As previously covered, the fixed mortgage rates charged by most lenders were unjustifiably high in Q4 2022 being way above what the financial markets suggested they should be. The SONIA (Sterling Overnight Index Average) swap rates widely used by lenders to hedge fixed rate mortgage risk have continued to fall.

In November, the best buy 2- and 5- year fixed rates were both above 5% and our prediction was that they would reduce to below 5% by Christmas which proved to be the case. There have been further reductions in mortgage rates since the start of the year and given that Swaps have continued to fall, and lenders have started to compete for business again I expect to see 5-year fixes below 4% by the end of March with 2-year fixes around 4.3%.

Top Tip - Borrowers booking in mortgage products now should ensure that the lender allows you to book a new product at a lower rate if one becomes available prior to completion. This is not routinely available across all lenders.

| November | Today | |

|---|---|---|

| 2-Year | 4.30% | 4.10% |

| 3-Year | 4.12% | 3.87% |

| 5-Year | 3.85% | 3.62% |

| November | Today | March Estimate | |

|---|---|---|---|

| 2-Year | 5.50% | 4.70% | 4.30% |

| 3-Year | 5.49% | 4.60% | 4.15% |

| 5-Year | 5.26% | 4.39% | 3.95% |

Housing Market

Transaction volumes are expected to fall to around 870k this year which is over 300k below the pre-pandemic norm of 1.20m. This drop follows two stellar years for the industry where transaction numbers were boosted by a very generous stamp duty incentive and high levels of demand following the lifting of lockdown restrictions and near zero interest rates. Much has changed since the start of 2022 with the cost of living crisis, high levels of inflation and far higher mortgages rates which all point towards lower levels of demand and the return of a ‘buyers’ market as a reduction in transaction volumes would usually correlate with a fall in prices.

| 2023 | 2024 | 2025 | 2026 | |

|---|---|---|---|---|

| First Time Buyers | 200k | 250k | 320k | 320k |

| Home Movers | 270k | 300k | 330k | 330k |

| Mortgaged Buy-to-Let | 40k | 50k | 60k | 60k |

| Cash Buyers | 360k | 400k | 400k | 400k |

| Total | 870k | 1.0m | 1.1m | 1.1m |

Will House Prices Crash?

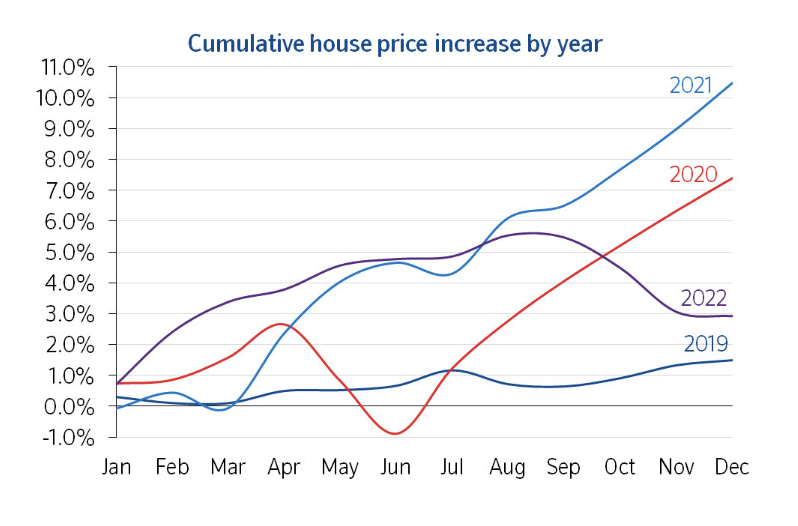

This depends on what you call a crash. In the early 90s and late 2000s, prices fell at least 20% but I think this time around the predictions of around an 8%-10% fall suggested by the largest lender Halifax (Lloyds Banking Group) and renowned Estate Agency Savills are about right. These need to be read in the context of a cumulative 20% + increase in prices from 2020-2022 as illustrated in Nationwide’s House Price Index. It's fair to say that a fall of 8%-10% back to April 2021 prices represents a correction rather than a crash, and from what I can see from deals currently being agreed this correction has already taken place and the house price indexes are yet to catch up due to the lag in the way they collect their data.

For house prices to crash (fall 20%), best buy mortgage rates would have had to settle above 5.5%, but now that it’s clear they are settling below 4.5% will put a floor on price falls particularly as unemployment remains low and greater levels of lender forbearance will prevent many of the forced sales that we have seen in previous downturns. Furthermore, underwriting standards in the last decade have been far more robust than prior to the financial crisis with all borrowers having to pass affordability tests where payments were stress tested at much higher interest rates. Borrowers who purchased at the top of the market should not be overly concerned as the vast majority will have taken out mortgage products at much lower rates than are available now, hence they're compensated for a fall in prices by having a lower monthly interest payment.

Negotiating Sale and Purchase Prices

When negotiating the sale price, vendors must forget what their property may have been worth at the top of the market in Q2 2022 and accept that the increased cost of living and higher mortgage rates has limited borrowing capacity and hence prices have adjusted. Buyers currently hold most of the cards and right now have the best opportunity to purchase at a discount since 2009, but should not overplay their hand as if mortgage rates continue to fall as anticipated then there will be a lot more buyers competing for property by the Spring.

How Can Jordan Lynch Help?

If you are purchasing a new property, the process can take several months and if we arrange your mortgage, we will constantly review your product right up to completion to ensure that you obtain the lowest rate possible by the time you collect the keys. If you’re a homeowner and your mortgage product expires this year we will book the best available re- mortgage or retention product for you six months in advance but will ensure that this is a product that can be cancelled, so if more favourable products are launched in the interim period (likely to be the case) we will switch you to one of those prior to completion.

Very best wishes to you all for the year ahead.

Tim Lynch - Founder and CEO.